Most insurance nightmares don’t start with a hurricane or a tree crashing through the roof. They start with a minor roof problem that feels easy to ignore. A lifted shingle after a windstorm. A small flashing gap you spot from the driveway. No leak yet, no urgency, no reason to panic. Except that roofs don’t fail all at once. They fail quietly, over time, and insurance companies pay close attention to how long that timeline stretches.

This is where homeowners get blindsided. What should have been a quick, affordable repair turns into a denied or heavily reduced insurance claim months later. By the time stains show up inside or insulation starts holding moisture, insurers often argue the damage wasn’t sudden. They call it maintenance neglect. Wear and tear. Pre-existing conditions. And suddenly, you’re staring at tens of thousands of dollars in repairs you assumed would be covered.

This article breaks down how small roof issues spiral into insurance disputes, why adjusters draw a hard line between sudden damage and gradual deterioration, and what you can do at each stage to protect yourself. From the first drip to dealing with adjusters, public adjusters, and attorneys, you’ll see exactly where most homeowners lose leverage, and how to avoid making the same costly mistakes.

Key Takeaways

- A $150 fix for a few missing shingles in October 2024 can snowball into a $25,000+ insurance dispute by the next storm season if left unaddressed.

- Insurance companies often deny or drastically limit coverage when they can label damage as “wear and tear” or point to maintenance neglect.

- Fast action—photos, temporary tarps, and a roofer’s report within 24–72 hours—can make all the difference between full coverage and total denial.

- Understanding the gap between what insurers call a covered peril versus gradual deterioration is critical to protecting your claim.

- This article walks you through each step from the first drip to dealing with adjusters and, if needed, bringing in an independent adjuster or attorney. Learn how to protect yourself after a severe storm as you navigate the insurance and repair process.

How a Tiny Roof Issue Turns Into a Massive Claim Problem

Picture this: A single shingle lifts during a March 2024 windstorm in Texas. You notice it from the driveway, make a mental note, and move on with your week. No leak. No visible damage inside. Seems harmless.

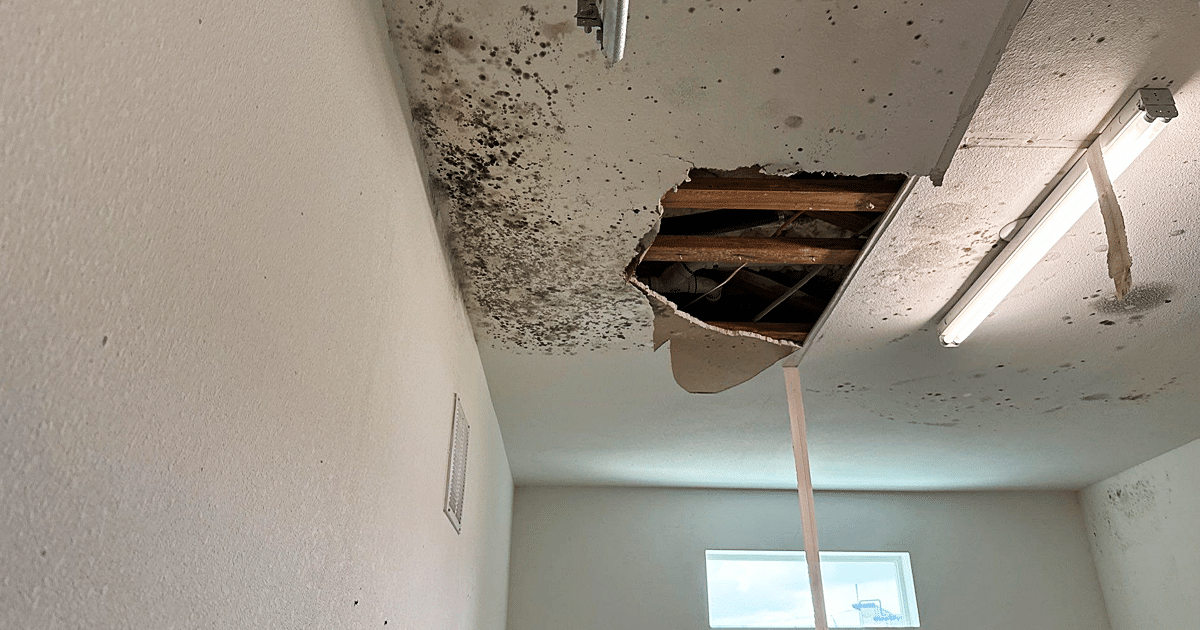

Three months later, a faint ceiling stain appears in the spare bedroom. By winter, that stain has spread across two rooms. The insulation in your attic is soaked. Mold growth has started behind the drywall. And when you finally call a roofing company, they’re talking about structural repairs to warped framing you didn’t even know existed.

Here’s where the insurance nightmare begins. The moment damage looks like it developed gradually, your insurance company has grounds to argue it wasn’t a sudden covered event. That one lifted shingle? Now it’s evidence of poor roof maintenance. That ceiling stain? Proof you ignored the problem. Your homeowner’s insurance policy distinguishes sharply between storm damage that happens in an instant and the kind of gradual deterioration that unfolds over months.

The cost progression tells the real story:

| Timeline | What Happened | Estimated Cost |

|---|---|---|

| Spring 2024 | Missing shingle, no visible interior damage | $150 patch |

| Summer 2024 | Faint stain, moisture detected in attic | $800–$1,200 inspection + minor roof repairs |

| Winter 2024 | Soaked insulation, visible mold, warped decking | $3,000–$5,000 interior repairs |

| Spring 2026 | Full structural damage discovered, extensive roof decay | $25,000–$40,000+ roof replacement + remediation |

What started as minor roof repairs has become a full-blown claim dispute—and the insurance adjuster is pointing to two years of neglect.

Water doesn’t wait for permission. It spreads sideways through your roof decking long before a single drop appears on your ceiling. By the time you see a stain, the damage behind your walls has likely been building for weeks or months.

In the first 30 days after a roof leak begins, water saturates the underlayment and starts wicking into your OSB decking. The material swells. Seams separate. Your R-38 attic insulation begins absorbing moisture like a sponge, losing its effectiveness and driving up your energy bills almost immediately.

By three months, fungal colonies have taken hold. Black mold spores thrive in the dark, humid environment between your roof and your living space. Rafters and trusses that were solid six months ago now show early signs of decay. The structural integrity of your roofing system is quietly eroding.

At the 12-month mark, you’re looking at a very different situation. What could have been a $200 patch now requires roof decking replacement, mold remediation, insulation removal, and potentially structural repairs to compromised framing. One loose flashing point can allow several gallons of water into your attic during every heavy rain—and that volume adds up faster than most homeowners realize.

The insurance implications are severe. Once an adjuster sees evidence of long-term water intrusion—discoloration patterns, wood decay, or mold colonies that clearly took months to develop—they have documentation to classify this as neglect rather than a covered event.

Where Insurance Draws the Line: Sudden Damage vs. Neglect

Your homeowner’s insurance policy is built around a fundamental distinction: it covers sudden, accidental perils, not slow deterioration.

When a 2025 hailstorm punches through your shingles in April, that’s a covered peril. When a tree limb crashes through your roof during a January 2024 ice storm, your policy should respond. Lightning strikes that loosen shingles, wind-driven debris that punctures your roofing materials, even the weight of accumulated snow and ice causing a partial collapse—these are the events homeowner’s insurance is designed to address.

But here’s where many homeowners get caught off guard. Your policy almost certainly contains exclusions for:

- Wear and tear – the natural aging of roofing materials over time

- Maintenance neglect – damage that resulted from ignored repairs

- Pre-existing conditions – problems that existed before the claimed storm event

- Gradual deterioration – slow decay from UV exposure, thermal cycling, or moisture

Old brittle shingles that finally gave way? That’s wear and tear. Cracked tiles that have obviously been deteriorating for years? Pre-existing damage. Rusted flashing that’s been leaking at low levels for multiple seasons? Maintenance neglect.

The practical effect is this: once an insurance adjuster can reasonably argue your roof was poorly maintained, they can deny all or part of your roof claim. This risk escalates dramatically for roofs past 15–20 years old, where insurers assume some level of age-related decline regardless of actual condition.

The language in standard policies is precise. If they can attribute your damage to anything other than a sudden, accidental event, your path to a fair settlement narrows considerably.

Insurance Tactics That Turn Small Roof Issues Into Nightmares

Insurance providers don’t always act in bad faith, but they do have financial incentives to minimize payouts—especially after major regional storms when claims flood in by the thousands.

Here are the tactics homeowners encounter most often:

Calling clear damage “cosmetic.” After a June 2024 hail event in the Midwest, some homeowners on the same street got full roof replacement approved while their neighbors were told identical damage was merely “cosmetic” and didn’t warrant coverage. The difference often came down to which adjuster showed up and how aggressively the homeowner pushed back.

Labeling storm damage as “age-related.” Damaged shingles that were clearly torn by wind get reclassified as “natural granule loss” or “thermal cracking.” The insurance adjuster points to your roof’s lifespan and argues the shingles would have failed anyway. Suddenly, your storm damage claim becomes a maintenance dispute.

Claiming the leak “must have been there for months.” If there’s any evidence of prior moisture—staining, slight discoloration, even dust patterns—adjusters may use it to argue the damage predates the recent storm. This shifts the cause from a covered peril to gradual deterioration.

Depreciation and payment schedules. Even when a claim is approved, many insurance companies pay actual cash value rather than replacement cost on older roofs. A 17-year-old roof might only receive 30–40% of what full roof replacement would cost, leaving homeowners to fund the gap themselves. In Texas alone, 47% of 2024 home insurance claims closed without payment, often due to high deductibles, depreciation, or disputed damage assessments.

Many homeowners don’t recognize these red flags until they’re already deep in a dispute. Understanding these tactics early helps you prepare a stronger case from day one.

Critical First 72 Hours: What to Do After You Spot a Minor Roof Problem

The actions you take in the first 1–3 days after discovering a roof leak or damage can determine whether your insurance claims process goes smoothly or turns into months of frustration.

Document everything immediately. Before you touch anything, grab your phone and take timestamped photos and videos from multiple angles. Capture the roof surface (if safely accessible), attic spaces, interior ceiling stains, baseboards, and any water on floors. Get these photos on the same day you discover the problem—dated evidence is your strongest protection against later disputes.

Stop active leaking, but don’t over-repair. Your next priority is mitigation, not permanent fixes. Use plastic sheeting, buckets, and carefully placed tarps to prevent further damage. Move furniture away from affected areas. Run fans or dehumidifiers to control moisture. Most insurance policies actually require you to take reasonable steps to limit further damage—and they typically cover the cost of emergency tarping and temporary measures.

Contact a roofing contractor and your insurer—quickly and in that order. Having a licensed roofer inspect the damage before the insurance adjuster arrives gives you an independent professional assessment. That contractor’s report becomes part of your evidence file and helps counter any attempt to minimize or reclassify your damage.

Create a simple timeline. Write down exactly when you first noticed the issue, what you observed, what steps you took, and when you made each call. This timeline becomes invaluable if there are later disputes about whether damage was sudden or gradual.

Prompt repairs—or at least prompt documentation and mitigation—show you acted responsibly. Delays give insurers ammunition to claim you contributed to the problem through neglect.

Building a Rock-Solid Roof Claim (Before It’s Denied)

The more organized your documentation, the harder it becomes for an insurance company to dismiss your claim. Think of your claim file as a legal case file—because if things go sideways, that’s exactly what it might become.

Assemble these elements before your adjuster visit:

- Dated photos showing the damage from multiple angles (exterior and interior)

- A licensed roofer’s inspection report with specific findings

- At least two detailed estimates for repair costs from reputable roofing contractors

- Receipts for any emergency work (tarping, water extraction, temporary repairs)

- A written damage timeline documenting every observation and action

Example timeline format:

| Date | Event |

|---|---|

| May 12, 2024 | First noticed ceiling stain in master bedroom |

| May 14, 2024 | Called ABC Roofing for inspection |

| May 16, 2024 | Roofer inspected; found lifted shingles and flashing damage; provided written report |

| May 18, 2024 | Filed claim with insurance; claim #12345 |

| May 20, 2024 | Heavy storm passed through area |

| May 22, 2024 | Adjuster visit scheduled for May 28 |

The key is having an independent roofing contractor’s report that specifically ties the damage to a recent storm or covered event—not just “old age.” Professional roofers experienced with insurance work know how to document the difference between storm damage and normal wear and tear. Their repair estimates should reference current labor costs, local building codes, and specific roofing materials needed.

When the adjuster arrives, you’re not starting from zero. You’re presenting an organized case that makes denial or lowballing significantly harder.

Working With Adjusters, Roofers, and (Sometimes) Public Adjusters

Understanding who the players are—and what motivates each of them—helps you navigate the claims process more effectively.

The company adjuster works for your insurance provider. Their job is to assess damage and determine what the policy covers. They’re not necessarily adversarial, but their employer has a financial interest in limiting payouts.

Your independent roofing contractor works for you. Choose professional roofers experienced with insurance claims who understand local building codes and can explain clearly why simple patch jobs won’t address underlying problems like compromised roof decking or structural damage.

A public adjuster is a licensed professional who represents homeowners—not insurers—in the claims process. They typically charge 10% of the settlement but often recover 200–300% more than homeowners negotiating alone, according to industry studies.

When the insurance adjuster visits:

- Be present for the entire inspection

- Share your photos, timeline, and contractor’s estimate upfront

- Walk them through every area of concern, including attic spaces

- Ask questions if they label anything as “cosmetic” or “pre-existing”

- Request their findings in writing

If your claim is denied or the offer seems drastically low compared to your contractor’s assessment, you have options. Request a reinspection. Escalate to a supervisor within the insurance company. If you’re still facing a stalemate after 30–60 days—especially with clear storm damage and an unfair denial—consulting a public adjuster or attorney becomes a reasonable next step.

The Encalade family in Colorado faced exactly this situation after a 2023 lightning strike. Their insurer initially offered $70,000; after litigation, the settlement reached $297,000. The gap between insurance scopes and what professional repairs actually require is often enormous.

How to Avoid an Insurance Nightmare in the First Place

Prevention and documentation are your best defenses against future disputes—especially as your roof ages past the 10–15 year mark where many insurance providers start applying stricter scrutiny.

Establish a regular inspection rhythm:

- Schedule professional roof inspections every 1–2 years

- Add an extra inspection after any significant hail or wind event in your region

- Don’t wait for visible leaks to catch minor issues early

Maintain a “roof file” that includes:

- Prior inspection reports (going back to 2020 or earlier if possible)

- Invoices and receipts for all roof repairs and maintenance

- Before-and-after photos of any work performed

- Documentation of when roofing materials were installed or replaced

Address minor issues immediately. Cracked tiles, missing shingles, loose flashing, and clogged gutters might seem like small annoyances, but they’re the exact evidence adjusters use to argue neglect. Timely repairs eliminate that argument before it starts.

Regular maintenance also extends your roof’s lifespan—potentially buying you years before you face the age-related coverage limits that many insurance companies impose on roofs past 15–20 years.

A documented, well-maintained roof puts you in the strongest possible position when a real storm hits. You can prove the damage was sudden, not gradual. You can show you fulfilled your maintenance obligations. And you can push back confidently against any attempt to deny claims based on neglect you never committed.

Frequently Asked Questions

Can insurance deny my roof claim because the damage looks old, even if a recent storm made it worse?

Insurance companies often argue “pre-existing” or “wear and tear” when they see signs of aging on a damaged roof. However, if a recent storm clearly aggravated an existing condition—shingles torn off during a March 2025 wind event, for example—they may still owe for the sudden portion of the damage.

The key is getting a licensed roofer’s written statement that distinguishes between old conditions and new storm-related damage. This documentation becomes your evidence when discussing the claim with your adjuster. Be aware that state insurance laws vary, so consulting a local attorney or public adjuster can clarify your rights in borderline situations.

What if my neighbors got full roof replacements from the same storm but my insurer only offered a small patch?

Different insurance providers—and even different adjusters within the same company—can reach wildly inconsistent conclusions, even for homes on the same street after the same June 2024 hailstorm.

If your offer seems disproportionately low, ask your roofing contractor to inspect your roof and compare damage with nearby homes. Submit their detailed report when requesting a reinspection from your insurer. If the company still refuses to budge, escalate internally through a supervisor or formal appeal process. Beyond that, bringing in an independent adjuster for their own damage assessment often reveals discrepancies the company adjuster missed or minimized.

Does filing a roof claim always raise my insurance rates or risk non-renewal?

One legitimate claim from a major event—like a declared 2023 hailstorm—doesn’t automatically guarantee a rate increase. Insurance companies do factor claim history into pricing decisions, but a single claim tied to widespread storm damage is typically viewed differently than multiple claims in a short period.

That said, some companies may choose not to renew policies after several large claims, especially on older roofs in high-risk regions. Before filing, weigh the size of the loss against your deductible and potential premium impact. Ask your agent directly how a claim might affect your future pricing—they can often provide guidance specific to your policy and claims history.

How old is “too old” for a roof when it comes to getting full replacement coverage?

Many insurers begin limiting payouts once asphalt shingle roofs reach 15–20 years of age. At that point, policies often shift from paying replacement cost (what it actually costs to install a new roof) to actual cash value (replacement cost minus depreciation). For a 20-year-old roof, that depreciation can reduce your payout to 30–40% of true repair costs.

Check your declarations page to see if your policy uses age-based payment schedules. If your roof was installed before 2005–2010 and you haven’t upgraded your coverage, you may face significant out-of-pocket costs after a covered event. Consider adding a replacement cost endorsement before your roof reaches that threshold—if your insurer offers it and the cost makes sense.

Should I fix a small leak myself before calling insurance?

Avoid major DIY roof work. Improper repairs or unlicensed work can give insurance providers grounds to reduce or deny coverage later. Even well-intentioned fixes can obscure evidence of the original damage, making it harder to prove your claim.

What you should do is take safe, temporary measures: interior buckets to catch water, plastic sheets to protect furnishings, and carefully placed tarps if you can access the roof without risk. Then call a licensed roofing contractor for a professional assessment.

Most importantly, document the original damage thoroughly with photos and video before any mitigation. That evidence is crucial for your claim file—and for proving the problem existed before you took steps to prevent leaks from causing further damage.

Will my insurance cover temporary tarping and emergency repairs after storm damage?

Most homeowner’s insurance policies include coverage for “reasonable and necessary” steps to prevent further damage after a covered event. Emergency tarping, water extraction, and temporary weatherproofing typically fall under this provision—and insurers usually reimburse these costs as part of your claim.

Save all receipts for emergency services. Take photos showing the temporary measures you put in place. Document when you called for help and what work was performed. These costs typically don’t count against your main claim amount; they’re separate line items for mitigation expenses. However, confirm this with your adjuster early in the process to avoid surprises.

How long do I have to file a roof damage claim after a storm?

Most insurance policies require you to report damage “promptly” or within a specific timeframe—often 30–90 days from when you discover the problem, though this varies by state and policy. Texas, for example, requires insurers to acknowledge claims within 15 days of notification.

Don’t wait for the damage to get worse before filing. Even if you’re not sure the repair costs will exceed your deductible, notify your insurance company within days of discovering damage. You can always decide not to pursue the claim later, but failing to report within policy deadlines can give insurers grounds for denial. Check your declarations page for specific notification requirements.

What’s the difference between a roofing contractor’s estimate and an insurance adjuster’s assessment?

A roofing contractor’s estimate typically reflects the full scope of work needed to properly repair your roof according to building codes and manufacturer specifications. This includes labor costs at current market rates, quality materials, and any necessary structural repairs discovered during inspection.

An insurance adjuster’s assessment determines what the policy will pay based on coverage limits, depreciation schedules, and their interpretation of what damage is “covered.” Adjusters often use software like Xactimate that may not reflect actual local contractor pricing or may underestimate the scope of hidden damage.

Significant gaps between these two numbers are common. Your contractor sees the physical reality of what needs repair; the adjuster evaluates what the policy contractually owes. When these diverge dramatically, you may need to negotiate, request a reinspection, or bring in a public adjuster to advocate for a fair settlement.

Can insurance force me to use their “preferred” roofing contractor?

No. You have the legal right to choose your own licensed roofing contractor for repairs, regardless of whether your insurance company maintains a “preferred vendor” or “network contractor” list.

Insurers may suggest contractors they’ve worked with before, and sometimes these relationships work smoothly. However, these contractors may also face pressure to minimize repair scopes to keep costs down—potentially leaving you with incomplete work. Choose a reputable local roofer with strong reviews, proper licensing, and experience handling insurance claims. Your contractor works for you, not your insurance provider.

What should I do if my insurance claim is denied?

First, request the denial in writing with specific reasons cited. Review your policy carefully to understand exactly what coverage you have and what exclusions apply. Then gather additional evidence: a second contractor’s assessment, photos showing storm damage versus pre-existing conditions, weather reports from the date of the claimed event, and your maintenance records.

File a formal appeal with your insurance company, escalating to a supervisor or claims manager. If the denial still seems unreasonable—especially for clear storm damage—consult a public adjuster or attorney who specializes in property insurance disputes. Many offer free initial consultations and can quickly assess whether you have grounds to challenge the decision. In some states, insurance bad faith laws provide additional leverage when companies deny valid claims without reasonable justification.